6 Investing Trends for 2026

February 27, 2026 • By David K. MacLeod, CFA, CFP®

Every January, our advisor team takes time to review how markets performed in the prior year, assess the economic landscape, and study the market areas where our clients are invested. That analysis helps guide how we manage portfolios, balancing long-term opportunities with risks.

We’ve seen strong returns since 2022’s lows, and we remain mindful that periods of volatility and market corrections are a normal part of investing.

Here are six investing trends that we’re watching in 2026:

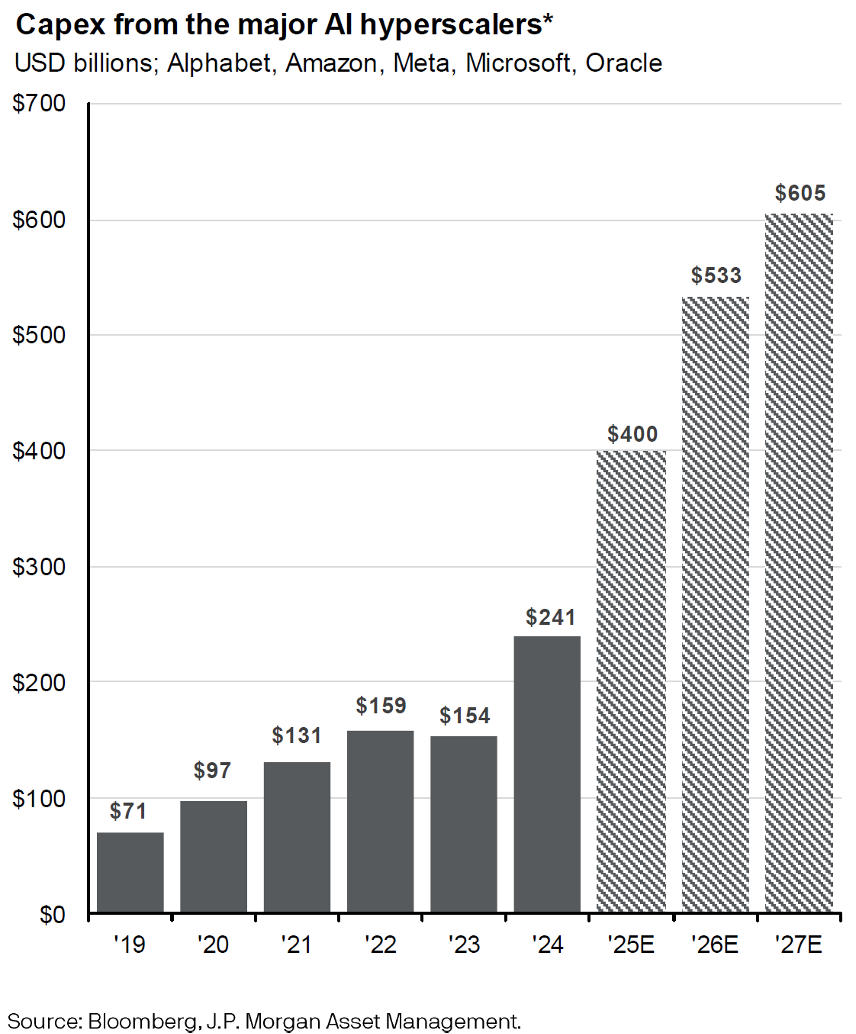

1. The AI Boom Is Fueling Economic Growth

You’ve undoubtedly heard a lot about artificial intelligence (AI) and have probably tried some of the four leading chatbots: ChatGPT, Claude, Copilot, and Gemini. AI has moved beyond a novel idea to real capital investment by leading U.S. technology companies. These companies are expected to spend over $500 billion on AI-related capital in 2026 and over $600 billion in 2027, as shown in the JP Morgan chart below. The investment includes building massive data centers and upgrading computer networks to improve the capabilities of AI models.

The investment is meaningfully contributing to economic growth. As a percentage of gross domestic product (GDP), last year’s AI capital spending was greater than the peak annual spending on the Manhattan Project, Apollo Project, and interstate highway system combined.

We want to carefully participate and have some exposure to growth sectors. But we never want client portfolios to depend too much on a single investment theme. Past capital spending booms, such as railroads and broadband internet, have led to busts.

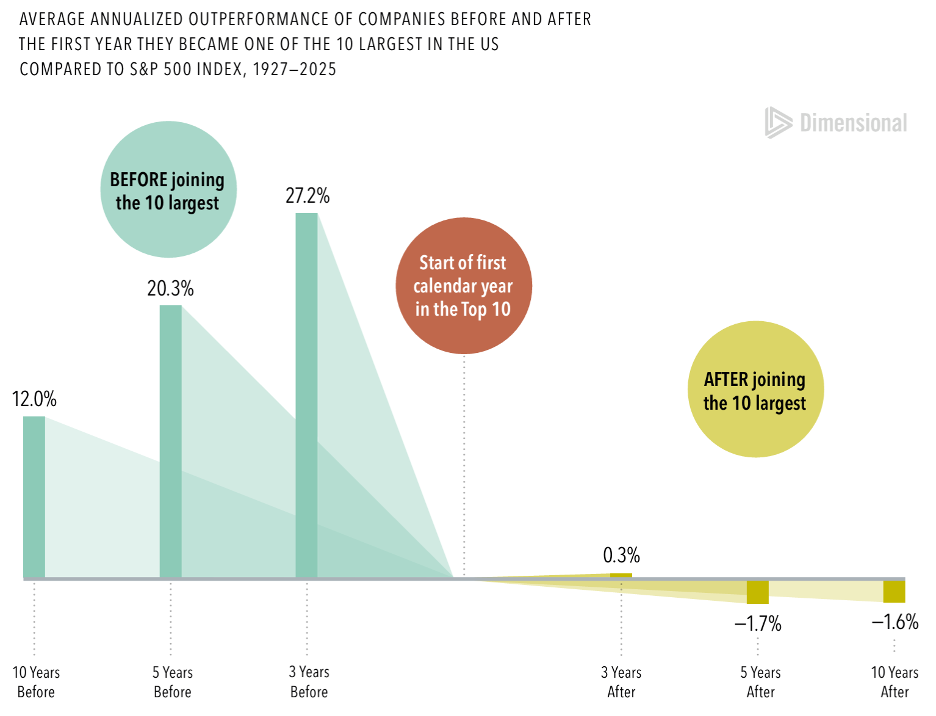

2. A Concentrated Group of Large U.S. Companies Dominates Leading Indexes

Over the past several years, U.S. and global stock market indexes have become more heavily concentrated in leading American technology companies. That doesn’t mean they are bad businesses. Many of these companies could benefit from the massive spending on AI, and they are profitable. But today’s top 10 companies are more expensive than the overall market and had slowing earnings growth in 2025.

The top 10 largest companies in the U.S. now represent 41% of the S&P 500 Index (compared to 17% ten years ago). Market leadership changes over time, so it’s concerning when very high expectations are placed on the leading companies. We wouldn’t be surprised to see a correction in the hottest stocks after the last few years of gains.

According to historical market research, as shown in the Dimensional chart below, companies have tended to perform poorly after reaching the top 10.

Source: Source: Dimensional Funds.

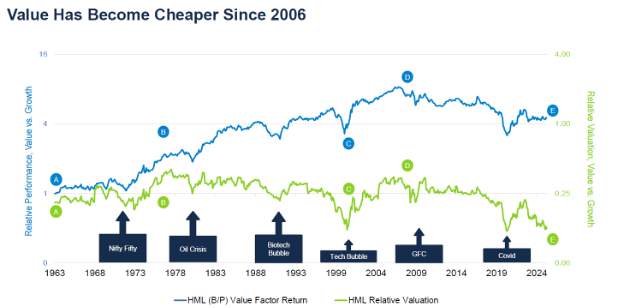

3. Value and International Stocks Have Attractive Valuations

While large U.S. companies have led the way for a while, value and international stocks have become more attractive due to more reasonable valuations. This reflects expectations that are more grounded, offering diversification benefits outside of the hottest top 10 stocks. Over the past year, value and international stocks performed very well alongside the leading U.S. companies.

The “Value vs. Growth” relative valuation chart from Research Affiliates below shows that value stocks have become cheaper relative to growth stocks over the past 20 years. This development bodes well for value-style investment returns if there’s a reversion to the long-term average. This isn’t a short-term prediction, but starting valuations have often proven to be predictive of long-term returns.

Source: Research Affiliates.

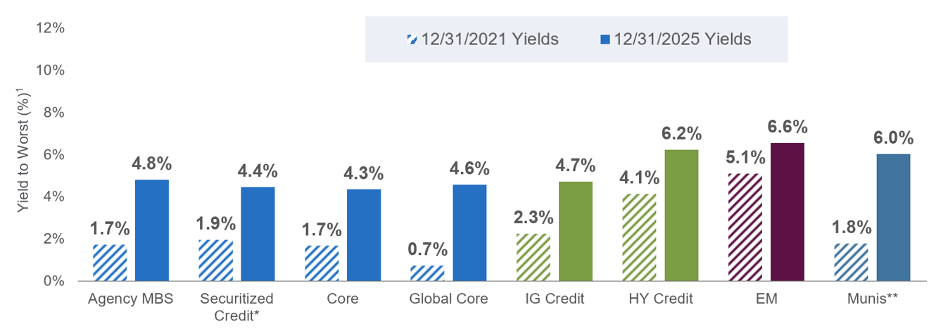

4. Bonds Are Back: Income and Stability Matter for When Volatility Returns

After many years of low bond yields, fixed income has become more compelling over the past few years. Bonds provide better portfolio stability during stock market corrections and economic recessions, and today’s yields are more attractive than they were last decade.

Per the PIMCO chart below, bond yields are significantly higher than they were four years ago across various fixed-income sectors. This indicates higher expected returns going forward. It doesn’t mean bonds are risk-free, but they do have a role in a balanced investment portfolio.

Source: PIMCO.

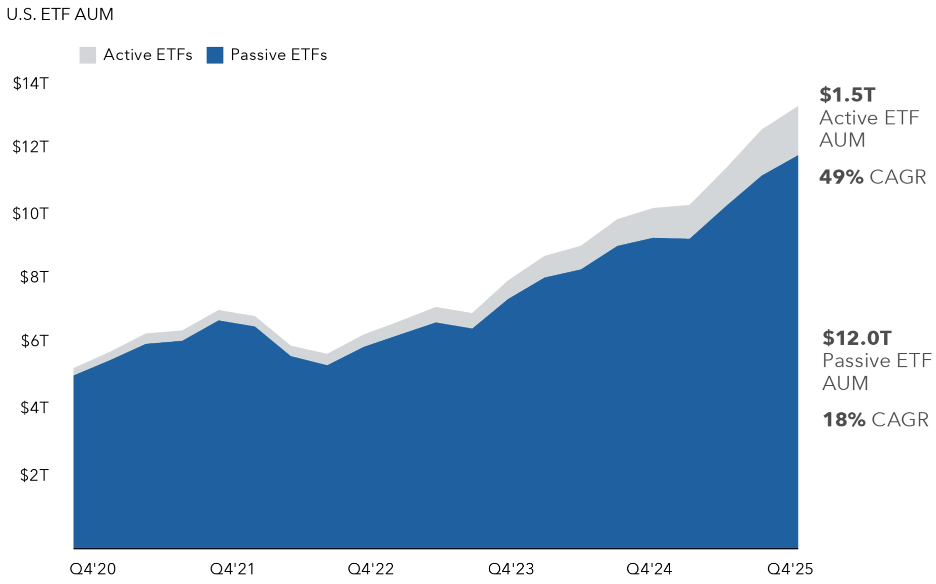

5. ETFs Are Becoming a Larger Part of Portfolios

We have recently shifted our recommendations toward more exchange-traded funds (ETFs). The reason for this change is the increasing availability of ETFs that align with our investing style, are more tax efficient, and are more cost-effective for client portfolios.

According to Capital Group, ETFs have grown to $13.5 trillion in assets under management, and the strong growth in assets is expected to continue through the end of the decade. Active ETFs managed by an active portfolio manager are growing faster than passive ETFs that closely track an underlying index.

Source: Capital Group.

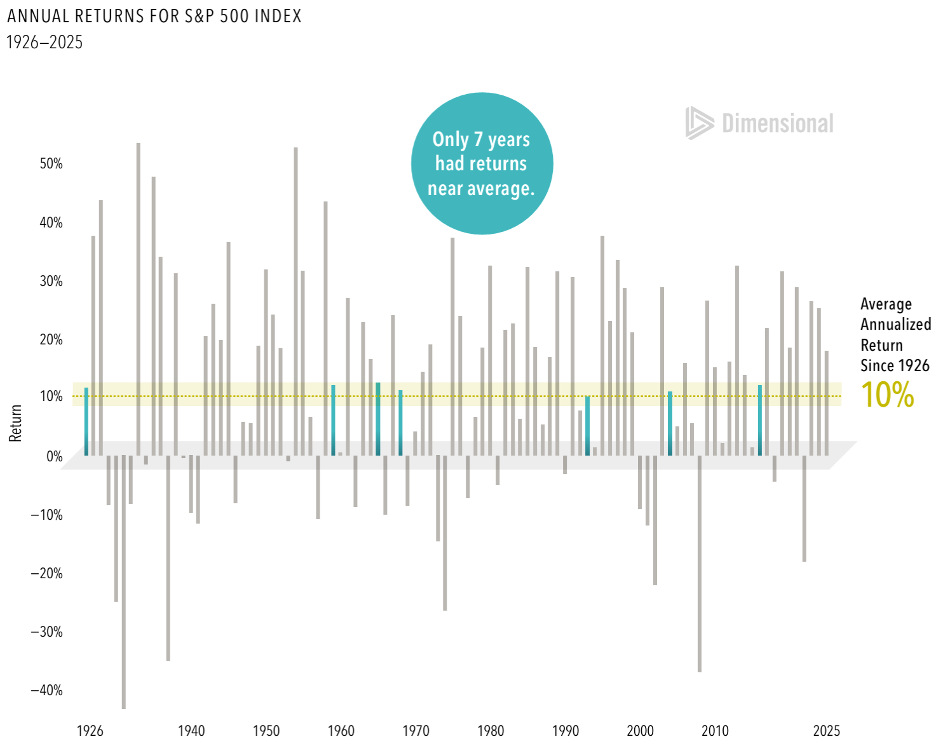

6. Sticking to the Plan Matters More Than Predicting What Happens in 2026

If history is a guide, the markets will react to plenty of surprises in 2026, such as wars, deficits, tariffs, policy shifts, and interest rate changes. We can’t control the causes or the effects of these variables. As the Dimensional chart below shows, over the past 100 years, the average stock market return has been 10%—but only seven out of 100 years saw returns close to that average. Dramatic swings up and down are the norm.

Source: Dimensional Funds.

We recommend focusing on the things you can control:

Sensible investment allocation

Regular rebalancing back to target allocations

Maintaining disciplined portfolio saving or spending levels

Revising your financial plan as your goals and needs change

When the next market correction comes, we’ll be ready to respond by rebalancing client portfolios. Practically, that will likely mean buying the asset classes that have dropped the most and trimming bond funds that have held up.

Please don’t hesitate to reach out to our advisor team if you have any questions about your portfolio. If you’d like to review your financial plan with us, feel free to contact our office to schedule an appointment.